Research Briefing

| Nov 20, 2023

Chip upcycle is a bright spot, albeit still a dim one

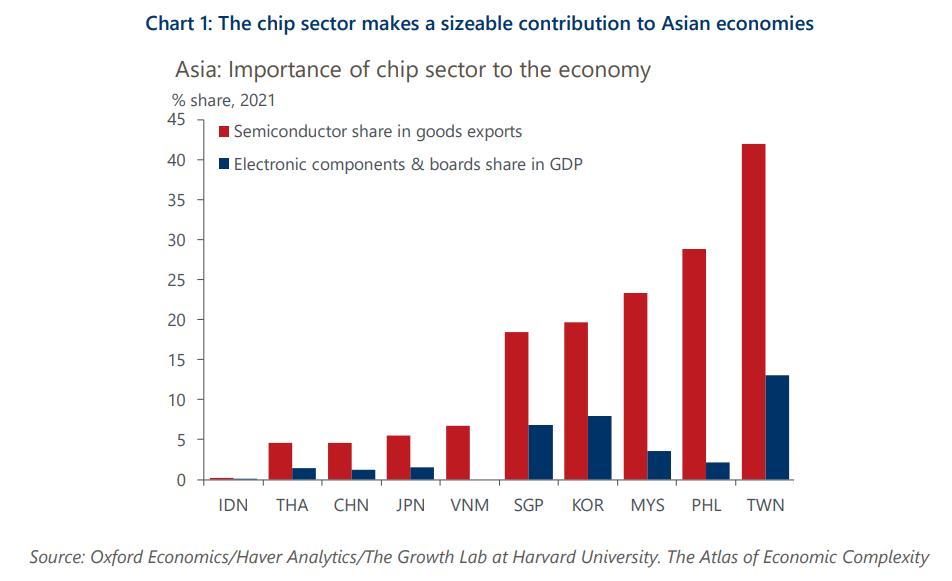

The chip sector is profoundly important for some Asian economies, given their role in the global semiconductor supply chain. As such, the ongoing recovery, albeit gradual, will provide some support to these economies amid the slowing global economy and tight domestic monetary policies.

What you will learn:

- Asia’s deeply integrated chip supply chain means the ongoing recovery in the sector will benefit the regional players evenly. The replacement demand for goods purchased during the pandemic will benefit memory and logic chips, as well as more diffuse chips that have a wider application.

- After turning earlier this year, we expect the chip-cycle upturn to be gradual. This is partly structural as chip cycles are rarely symmetrical, but there are additional headwinds this time.

- The slowing global economy will likely mute the replacement demand for goods, while accumulated inventory caused by the hoarding of chips during Covid will keep production relatively low. The normalisation in the automotive sector adds another obstacle.

- Although we think Asia’s position as the world’s chip-production hub will be little challenged for the foreseeable future, geopolitical conflicts and inward-looking policies are a risk.