Research Briefing

| Sep 5, 2023

After the post-pandemic slump, a steady climb back for Latin America

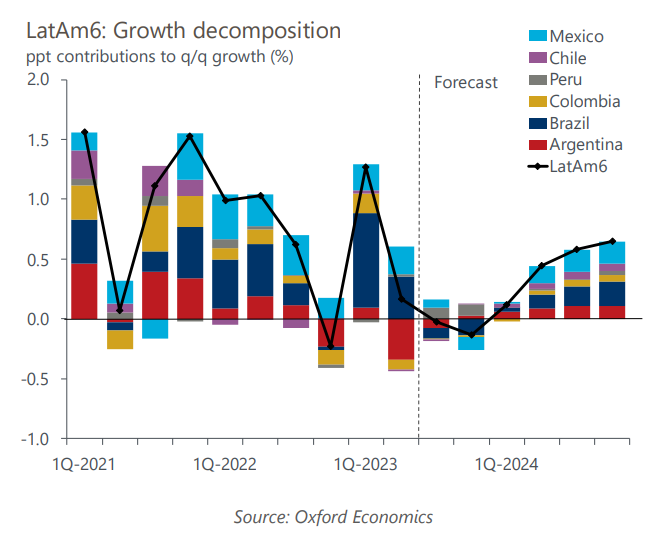

We expect Latin America’s six largest countries’ combined GDP to expand 0.8% next year, down from our 1.8% forecast for 2023 and the consensus’ 1.4%. The dissipation of idiosyncratic shocks and less restrictive domestic policies should support a broad regional recovery in 2024 from the recessions LatAm’s major economies are in or about to enter.

What you will learn:

- The disinflation process will continue, but inflation will not return to central bank targets until early 2025. Supply shocks and aggregate demand pressures are fading, but volatility in commodity prices poses upside risks.

- The monetary normalization cycle has started in the region, well ahead of advanced economies and other emerging market peers. Central banks in Chile and Brazil are paving the way, and Peru and Colombia are likely to follow. But Mexico will be the last to cut rates.

- The medium-term outlook for the region is still positive but growth is capped by low investment and significant political risk. Most countries have rebounded to potential output trends, but Peru and Mexico have not, and the lack of policy support will likely extend the scarring left by the pandemic.