Weak world trade still a drag on global growth

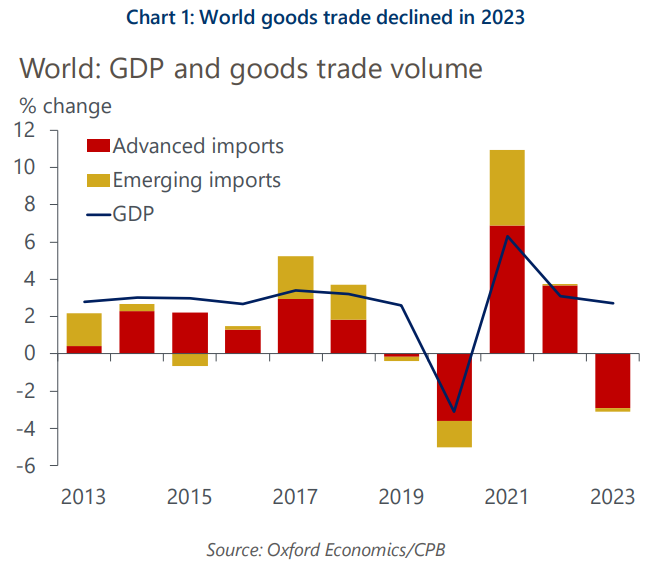

World goods trade declined in 2023, reversing the trend of 2022. This development points to the resumption of the decade-long pattern of slow global trade growth relative to GDP. Recent trade trends imply downside growth risks for 2024 and the longer-term outlook still looks to be one characterised by ‘slowbalisation’, especially with protectionism a rising issue.

What you will learn:

- Weakness in goods trade in 2023 was centred in advanced economies, especially Europe and Japan. Our survey-based indicator suggests global goods trade growth will remain stagnant into mid-2024, presenting a downside risk to our baseline trade forecasts.

- Muted external demand growth is one of the factors behind China once again starting to export disinflation to the world via lower export prices. The impact is not yet very large, but it could fuel protectionist pressures.

- Trade restrictions, in part linked to geopolitics, are a growing risk to long-term trade growth. The stock of restrictions has risen notably since 2016-2017 and there is a major new issue in the shape of distortionary industrial policies.

- The main area of fragmentation in the world trade system remains the US-China trade relationship. There are some signs this is spreading, however, such as the striking collapse of FDI into China in 2023, which implies lower trade in the future.

Tags:

Related Posts

Post

A reality check on the status of RMB internationalisation

The recent geopolitical shocks and abrupt US policy shifts have heightened concerns about the stability of the dollar-centric global financial system and strengthened the perceived need for diversification.

Find Out More

Post

China and AI underpin stronger global trade outlook

Global trade is set for a stronger-than-expected rebound, supported by lower US tariffs, continued AI-driven investment, and China’s renewed export push. Our latest forecasts show upgrades to both nominal and volume trade growth in 2025–26, even as legal uncertainty surrounding US tariff mechanisms and evolving geopolitical dynamics pose risks to the outlook.

Find Out More

Post

Tariffs take a toll despite easing trade hostilities

Global tradeflows remain under pressure despite easing tariff tensions. Recent US–China agreements reduce select import taxes and support China’s 2026 outlook, yet US imports continue to fall and supply chains pivot toward Asia and Europe. Containerised trade is set to expand, while bulk shipments soften alongside weaker industrial demand.

Find Out More