Research Briefing

| Jul 14, 2023

US supply-chain logjams are quickly fading

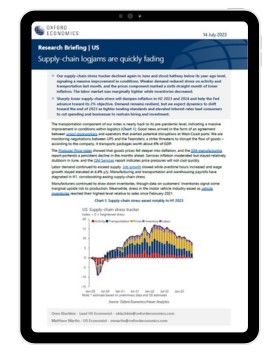

Our supply-chain stress tracker declined again in June and stood halfway below its year-ago level, signaling a massive improvement in conditions. Weaker demand reduced stress on activity and transportation last month, and the prices component marked a sixth straight month of lower inflation. The labor market was marginally tighter while inventories decreased.

What you will learn:

- Sharply lower supply-chain stress will dampen inflation in H2 2023 and 2024 and help the Fed advance toward its 2% objective. Demand remains resilient, but we expect dynamics to shift toward the end of 2023 as tighter lending standards and elevated interest rates lead consumers to cut spending and businesses to restrain hiring and investment.