Research Briefing

| Dec 13, 2023

The path of monetary policy will shape the growth outlook of Indonesia

Indonesia’s domestic demand has proved surprisingly resilient to monetary tightening in 2023, prompting multiple upgrades to our growth forecast this year. However, we still expect the impact of monetary tightening will feed through to growth eventually.

What you will learn:

- Two key shifts will influence the monetary policy path in 2024. Indonesia’s current account dipped into deficit in Q2, and we don’t expect it to revert to surplus anytime soon. Lower commodity prices, as well as the contrasting picture between relatively resilient domestic demand and a soft external sector will suppress the external balance.

- Meanwhile, the pace of rupiah weakening might moderate, but we expect the depreciating trend to continue. While the rupiah has bounced back a little in the last month, we suspect the main driver – lower US yields – will partly reverse given market pricing for rate cuts in the US is likely overdone.

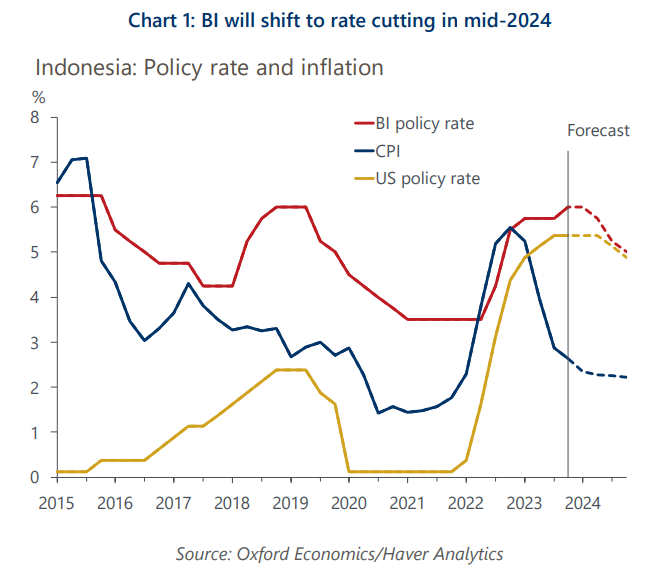

- After a surprise hike in October, Bank Indonesia stayed put in November and we think will remain on hold for some time.

- We think Indonesia’s growth will remain below-trend in 2024 given the impact from past monetary tightening and a weak global economic backdrop.