Research Briefing

| Feb 19, 2024

The costs and eventual benefits of smooth decarbonisation in ASEAN

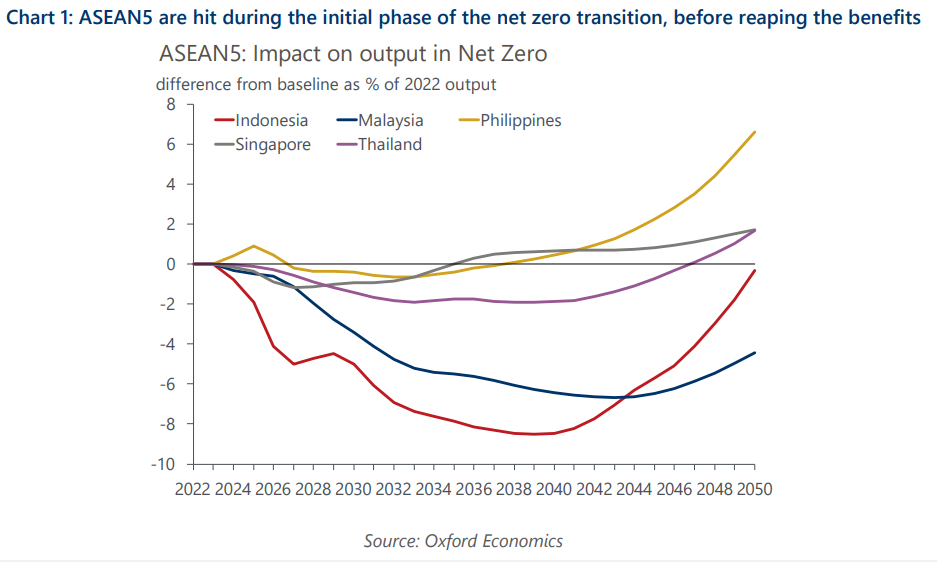

Reaching net zero carbon emissions by 2050 would likely have a larger impact on economic activity initially in ASEAN5 countries than more gradual decarbonisation. But our modelling suggests the gap would narrow in later years and turn positive in most places approaching 2050.

What you will learn:

- The initial costs of decarbonisation largely stem from higher energy costs as carbon taxes are levied, which businesses will have to bear as the switch to renewables takes time. Offsetting benefits are likely to accrue in later time periods from the avoided impacts of climate change, declining energy prices, and higher green investment.

- Net energy exporters – Malaysia and Indonesia – are likely to face the biggest upfront costs. Indonesia looks set to have a particularly tough time at the start given its high reliance on coal in the energy mix. But over the longer term, it should eventually see a larger benefit than Malaysia due to higher growth in public services and declining energy costs.

- Thailand is in the middle of the pack. It has a high energy intensity, though the impact is likely to be offset by lower reliance on coal.

- Initial costs are more limited in Singapore and the Philippines due to low energy intensity – both will see economic benefits from the transition during the 2030s. The Philippines stands out with the highest output above our baseline in the long term due to its high potential in electric power generation and distribution.