Research Briefing

| Oct 3, 2022

Shifting Asian supply chains amid ongoing US-China frictions

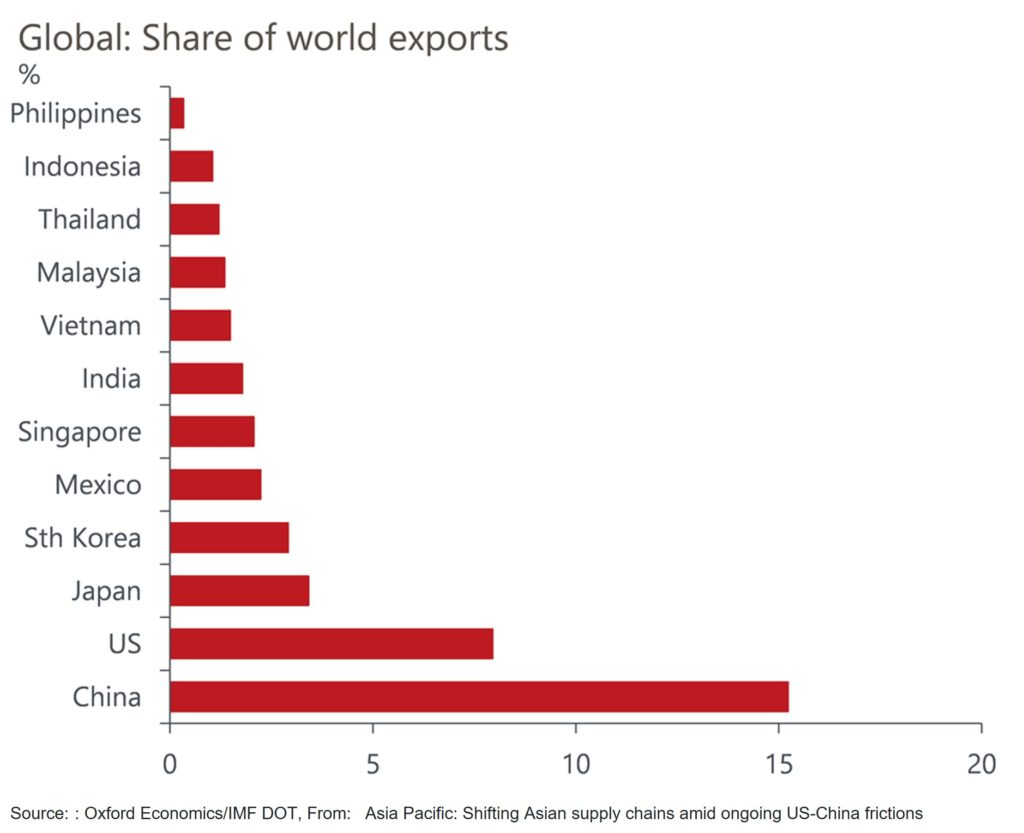

Manufacturing hubs in South East Asia are set to benefit from firms hedging against ongoing US-China frictions, in our view, and ASEAN countries will continue to be attractive destinations for investment.

What you will learn:

- We expect Vietnam in particular to be a big beneficiary given its proximity to China, participation in free trade agreements, and low-cost advantage.

- Although we expect ASEAN to become an increasing source of global manufacturing and goods exports, breaking the global and regional dependency on China would require a significant drop in the reliance on backward integration with Chinese industry. There is little evidence of this yet.

- We think it’s more likely that firms will opt for a ‘China plus-one’ strategy, reducing their dependency on China only marginally. We expect this strategy, along with growing domestic markets in ASEAN and China, will strengthen intra-regional economic linkages.