Research Briefing

| Mar 12, 2024

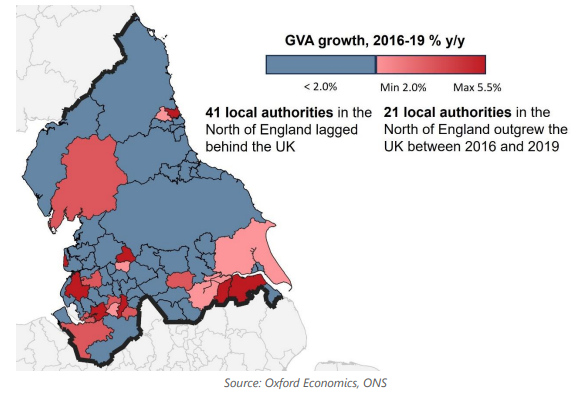

Only a few northern economies will outperform the UK

While economic growth in the north of England is generally below the UK average, that is not always the case. In 2016-19, 21 northern local authority districts, or a third of the total, outpaced the UK for GVA growth, some of them substantially, and with the City of Manchester leading. Unfortunately, we forecast that the number will fall to just seven in the 2024-28 period.

What you will learn:

- The City of Manchester led the northern GVA growth league in 2016-19, while its Greater Manchester neighbours, Stockport and Salford, were both in the top ten. Salford managed that despite a decline in productivity, whereas the City of Manchester saw balanced growth, reflecting increasing numbers of high-value, knowledge economy workers. That is a trick that few northern cities are really pulling off.

- Indeed, it is apparent that the better performing parts of the north pre-pandemic had very different drivers, with no over-arching pattern of success.

- To address poor economic performance, Combined Authorities spanning local areas are intended to take advantage of local linkages, so that by pooling powers, success in one place can produce success in neighbouring local economies. Greater Manchester provides an example of that working, but not perhaps for the combined authority area as a whole, or at least not yet.

- Indeed, our own forecasts do not assume that combined authority status will have a material impact on local area economic performance.