Research Briefing

| Mar 25, 2024

New ECB framework a versatile toolkit for uncertain times

The European Central Bank’s updated monetary policy framework retains key advantages of the previous system and in our view is well-tailored to the eurozone’s bank-dominated financial infrastructure. It also gives the ECB a versatile toolkit allowing it to react flexibly to episodes of market stress.

What you will learn:

- An update to the way the ECB provides liquidity to the financial system was needed as its supply of reserves is being drawn down through quantitative tightening. In particular, the ECB needed to choose between the pre-crisis ‘corridor’ system in which reserves are scarce or stick to the current ‘floor’ system of ample reserves.

- The ECB opted for a demand-driven floor system, whereby banks will make use of a lending facility to ensure that reserve holdings match operational, liquidity and risk management needs. A key advantage of this system is that it limits volatility and prevents sudden spikes in market rates.

- In addition, the ECB’s decision to narrow the spread between the deposit and refinancing rates to 15bps implies a non-negligible “cost of carry” for banks and is meant to resuscitate a largely dormant interbank lending market.

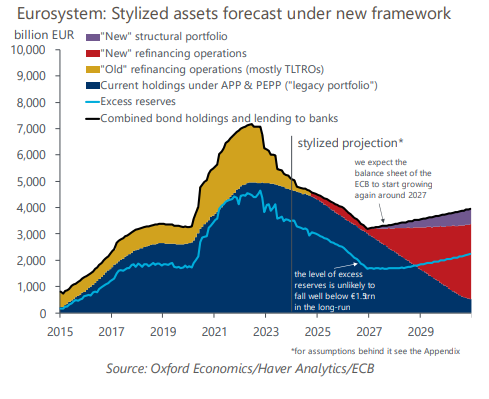

- As a result of the changes, the supply of safe assets should be larger, making collateral shortages less of a risk. The ECB’s new structural portfolio will also allow the central bank to affect market conditions for public and private assets.

- The ECB decided to keep the minimum reserve requirement (MRR) at 1%. While this decision will postpone the return of the eurosystem to profitability, it was probably needed to avoid the hit to liquidity in vulnerable banking jurisdictions, particularly Italy’s.