Research Briefing

| Apr 15, 2024

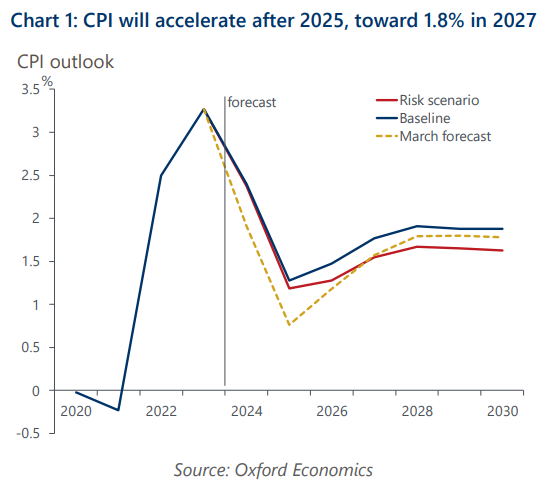

Japan inflation to rise to 1.8%, but downside risks are high

Reflecting a surprisingly strong Spring Negotiation result and weaker yen assumption, we have upgraded our baseline wage and inflation forecasts. We now project higher wage settlements will push inflation towards 1.8% by 2027. Uncertainty is high, however.

What you will learn:

- We anticipate the final outcome of the Spring Negotiation this year will likely be a wage rise of around 4.5% or more – much higher than last year’s 3.6%. We upgraded our wage projections for the next few years to reflect more aggressive wage-setting behaviour by top-tier firms.

- The main downside risk to our outlook is the sustainability of wage increases by SMEs. Another downside risk is disappointing demand growth, which will constrain pricing power.

- In our downside scenario, which assumes that these inter-related downside risks materialise, we project the CPI inflation rate would stabilise at 1.6% in 2027.