Research Briefing

| Apr 16, 2024

Indonesia rate cuts will bolster credit demand, with pockets of risks

We forecast Bank Indonesia will start cutting its policy rate in Q2, which will provide a cyclical tailwind for credit growth and consequently domestic demand, as lower real lending rates will help boost loan demand.

What you will learn:

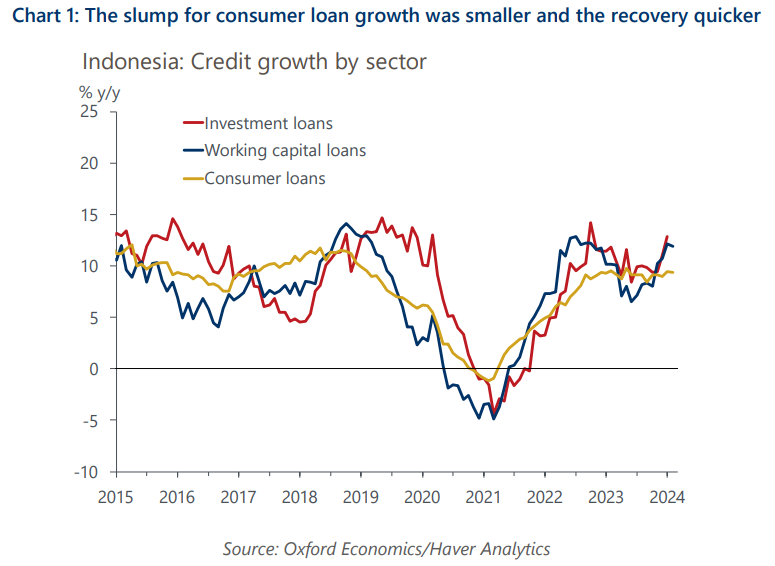

- Demand for consumer loans remains historically high as households struggle to make ends meet due to low earnings, even though they now face less pressure from high inflation. We think labour market conditions will remain poor this year, so loan demand will likely remain strong, further boosted by declining real rates.

- Business loan demand is also healthy given plateauing real lending rates, but the growth outlook depends on the usage. Improving liquidity will reduce demand for working capital loans, while the strong domestic sector will bolster investment loan demand. However, the soft external sector will likely be a drag.

- Initial signs of downside risk are emerging. The nonperforming loans (NPLs) ratio for consumers is rising, though is still at a low level. Similarly, the share of household income allocated towards debt repayment is rising from a depressed level, suggesting at least some households are starting to suffer as loans come due.

- There are also structural headwinds buffeting growth beyond the near term, such as the lack of financial deepening, which would require more fundamental solutions.

- Aside from rising NPLs for consumers, banks’ liquidity is low, which could be a barrier to extending long-term investment loans. But banks’ lending standards appear relatively loose compared to history given ample capital buffers, vast deposits, and high provision for losses.