Research Briefing

| Mar 6, 2024

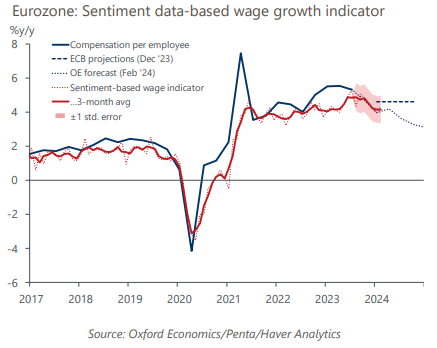

Eurozone: New wage growth data suggest no need to delay rate cuts

Our sentiment data suggests that the ECB’s worries about sticky inflation driven by strong wage growth are misplaced. The sentiment data-based nowcast, which allows us to track labour market developments in near-real time, suggests that pay growth continued to cool at the start of 2024 and is running below the ECB’s projections.

What you will learn:

- We think the ECB overstates the risk of sticky wages. We view current wage growth mainly as a catch up on previous real income losses and a prerequisite for a consumer recovery. The risk of sticky wage growth close to 4% y/y is limited in the medium term, in our view.

- Labour market resilience, including surprisingly strong employment growth, has propped up wage growth. But our labour market sentiment index suggests that resilience is fading, a point substantiated by falling hiring intentions. Sentiment around wage-related topics specifically is also at contained levels.

- We forecast earnings growth to slow to 3.2% by the end of the year and productivity growth gradually picking up. This will help to offset inflationary pressures from nominal wage growth, making it consistent with the ECB’s 2% target by year-end. We still expect 125bps worth of rate cuts in 2024 overall.