Research Briefing

| Apr 17, 2024

Eurozone: Little sign of harm from the Red Sea disruptions

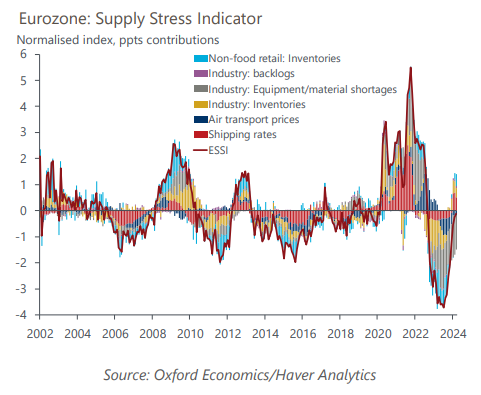

The impact of Red Sea shipping disruption on the eurozone economy continues to be limited, in line with our baseline view. Our new Eurozone Supply Stress Indicator suggests that supply pressures have returned to normal following a period of easing in 2023.

What you will learn:

- In our original assessment, we had assumed shipping rates on the affected routes would rise around 200% and settle at this level for six months. Encouragingly, shipping rates have eased slightly from January peaks. Moreover, early price and firm survey data point to a limited and scattered negative impact so far.

- Given the slow pass-through into domestic prices, we expect the impact of disruptions to peak towards the end of the year. But wider disinflation pressures stemming from falling energy prices and subdued demand mean we expect goods inflation to remain low, and the disruption shouldn’t prevent the ECB from cutting rates.

- Adverse risks haven’t dissipated, though. So far, we haven’t seen any clear signs that missing inputs are causing supply disruption or widespread production shutdowns, but these might show up later. Similarly, while most shipping companies now avoid the Red Sea, an escalation in attacks would have negative knock-on effects on both output and prices in the eurozone.