Research Briefing

| Dec 20, 2023

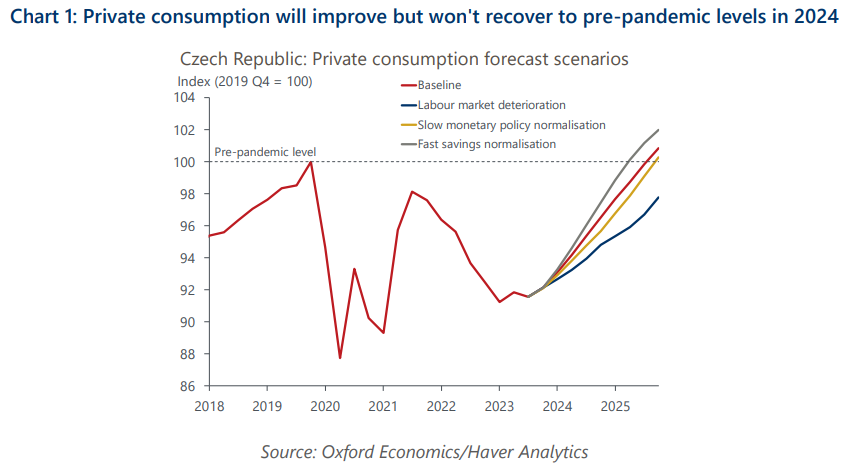

Czech Republic: Normalised savings will lift, not turbo-charge consumption

A plunge in consumer spending in 2022-23 has been a key factor behind the poor performance of the Czech economy. A recovery in consumption hinges on households normalising their elevated savings rate. We think this will be a gradual process, closely tied to monetary policy normalisation.

What you will learn:

- We think the recent rise in households’ savings rate was mainly due to the sharp rise in interest rates which makes savings more attractive. Weak confidence or precautionary motives have played a smaller role.

- A simple return of the savings rate to the pre-pandemic average could be a strong boost for consumption, though insufficient on its own to fully recover lost consumption. Also, households’ saving and spending decisions don’t happen in isolation, and wider economic conditions aren’t conducive to splurging.

- This is why we are sceptical about a rapid normalisation in savings. Although we think the central bank will have to catch up next year, policy rate normalisation will be sequential. Similarly, even as real earnings resume growing, uncertainty is unlikely to dissipate – if anything, deteriorating external demand and growing cracks in the labour market suggest the opposite.