Research Briefing

| Apr 29, 2024

BoJ likely to end zero interest rates in autumn

As expected, the BoJ maintained its policy rate at 0%-0.1% at Friday’s meeting. With more confidence on the ongoing wage-driven inflation dynamics and a strong appetite for policy normalisation, the BoJ looks more likely to end its zero-interest rate policy in the autumn.

What you will learn:

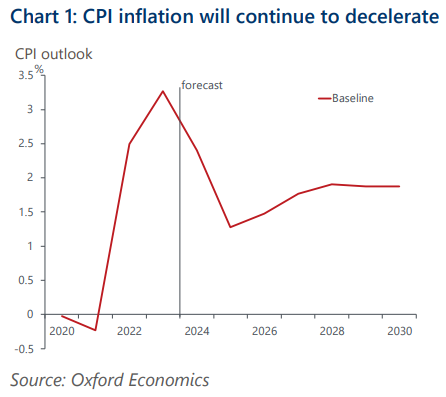

- The median CPI (excluding fresh food and energy) forecast in the Quarterly Outlook Report was unchanged at 1.9% for FY2024 and 2025. The figure for FY2026 was 2.1%, showcasing the BoJ’s confidence that it will achieve the 2% inflation target in coming years.

- The BoJ has increasingly stressed that monetary policy is data dependent. The wage settlement for SMEs at the Spring Negotiation continues to provide upside surprises.

- Assuming the recovery in real incomes and consumption is confirmed in the summer, the BoJ will likely raise its policy rate, arguing that the probability of meeting the 2% target has risen.

- We still project that the BoJ will cautiously raise its policy rate to 1% by 2028. The risk that 1% won’t be reached is also still significant due to the huge downside risks in the medium-term price outlook, especially the sustainability of wage rises and SMEs’ pricing power.