Research Briefing

| Jan 20, 2023

Receding US supply-chain pressures offer new year cheer

Supply–chain stress continues to recede, boding well for inflation and lending some upside risk to our near-term growth outlook. Odds are it will take time for the positive impact to work through the economy, but the effects of the pandemic and other recent shocks on supply-chains are clearly fading.

What you will learn:

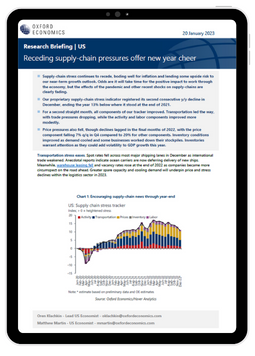

- Our proprietary supply-chain stress indicator registered its second consecutive y/y decline in December, ending the year 13% below where it stood at the end of 2021.

- For a second straight month, all components of our tracker improved. Transportation led the way, with trade pressures dropping, while the activity and labor components improved more modestly.

- Price pressures also fell, though declines lagged in the final months of 2022, with the price component falling 7% q/q in Q4 compared to 20% for other components. Inventory conditions improved as demand cooled and some businesses worked down their stockpiles. Inventories warrant attention as they could add volatility to GDP growth this year.

Tags:

Related Services

Service

US Forecasting Service

Access to short- and long-term analysis, scenarios and forecasts for the US economy.

Find Out More